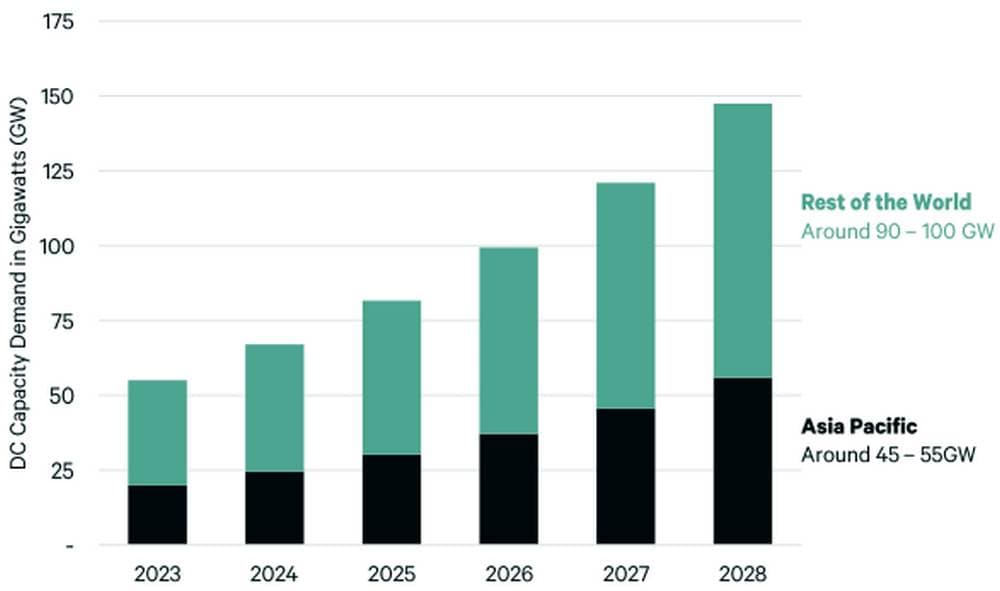

According to CBRE’s latest research, the rapidly growing demand for data centres in Asia Pacific is driven by the surge in artificial intelligence (AI) adoption and cloud services.

Figure 1: Estimated global data centre demand

Despite expectations of a doubling in data centre supply over the next three years, a significant shortage of 15–25 gigawatts of power is anticipated by 2028 due to inadequate infrastructure and a lack of AI-ready facilities.

The report highlights that AI-focused data centres require more than double the power density per server rack compared to traditional ones. This increased demand necessitates advanced cooling systems, enhanced floor loading capacities, and heightened sensitivity to network latency and bandwidth.

Many existing data centre projects were designed before the AI revolution, leaving a gap in facilities equipped to handle these advanced workloads.

Investment in data centres remains robust, with direct investment volumes reaching US$4.7 billion in 2024, according to CBRE and MSCI research. Early 2025 has seen continued activity as operators look to repurpose stabilised assets, despite challenges such as inadequate power supply and community opposition.

Tom Fillmore, executive director for Data Centres at CBRE, emphasised the need for investors to focus on advanced data centre assets to capitalise on AI workload growth. “Prioritising mergers and acquisitions, as well as equity investments in operators with a strong development pipeline, will be key to achieving scalability, especially for power-ready projects,” he stated.

The data centre sector's strong fundamentals are expected to provide ample investment opportunities, whether through direct acquisition, new development, joint ventures, or platform investments. Newer, advanced assets are likely to attract increasing investment demand, leading to steady price appreciation.

Ada Choi, head of research for CBRE Asia Pacific, noted that the AI boom and the growing need for cloud services will continue to drive substantial demand for both co-location and hyperscale data centres. Developed markets like Japan, Australia, and Korea are expected to see heightened demand, with Singapore also attracting interest despite its supply constraints.