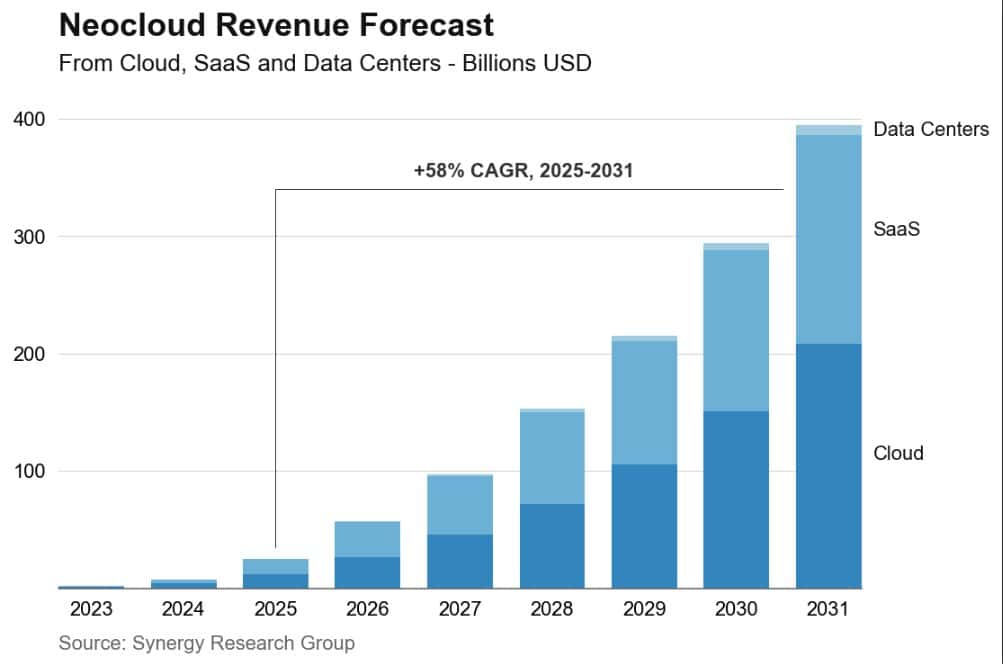

The neocloud market is experiencing unprecedented growth, projected to reach nearly $400 billion by 2031. This surge is primarily driven by the escalating demand for AI infrastructure, particularly for GPU-accelerated compute, which is outstripping the capacity of traditional cloud providers.

Neoclouds are emerging as a distinct category of cloud infrastructure, purpose-built to cater to the specific needs of AI workloads, offering services like GPU-as-a-Service (GPUaaS) and generative AI platforms.

Key players in this rapidly evolving landscape include CoreWeave, which is seen as a significant challenger to established hyperscale providers. Additionally, companies like OpenAI and Anthropic are carving out a niche as platform-centric providers, offering cloud-like access to foundational AI models and development environments.

These entities are collectively reshaping the competitive dynamics within the cloud ecosystem, blurring the lines between infrastructure and platform layers.

The growth of neoclouds is further propelled by structural constraints within traditional cloud supply chains. As the demand for GPU-intensive computing continues to climb, neocloud providers are capturing an increasing share of the fastest-growing market segments. This trend is prompting a fundamental realignment in the architecture of computation itself.

Jeremy Duke, founder and chief analyst at Synergy Research Group, noted, "What we are observing is not merely the emergence of a new class of cloud provider, but a deeper structural realignment in the architecture of computation itself. Traditional hyperscale systems were conceived around a form of generalized elasticity, whereas AI workloads impose far more rigid constraints—particularly around parallelism, locality and the concentration of compute. Neoclouds are, in effect, an architectural response to those constraints."

Companies such as CoreWeave, Crusoe, Core Scientific, Lambda, Nebius, and Nscale are at the forefront of this neocloud revolution. Their specialised focus on GPU-accelerated compute enables enhanced performance density, quicker deployment cycles, and more efficient scaling for AI workloads, positioning them as focused alternatives to traditional hyperscale providers like Amazon, Microsoft, and Google.

The market is characterised by significant investment and expansion. For instance, CoreWeave has secured substantial funding, including an $8.5 billion investment-grade financing facility, to scale its AI cloud platform and meet the growing demand from large-scale AI companies.

This financial backing underscores the confidence in the neocloud model, especially given the sustained demand for AI compute and strategic alliances with key AI players like NVIDIA and OpenAI.

The competitive landscape also includes platform-centric providers like OpenAI and Anthropic, who offer access to foundational models and AI development environments. While OpenAI has a broad consumer reach, Anthropic focuses on enterprise trust and safety, with a significant portion of its revenue derived from business customers.

These companies are investing heavily in compute power, with OpenAI expecting to spend $121 billion on computing power for AI research in 2028.

The neocloud market's trajectory suggests a sustained compound annual growth rate of 58%, indicating a robust and expanding sector poised to redefine the future of cloud infrastructure and AI computation.